Global Equity Investment Philosophy

Our philosophy is centred on the search for 'Future Quality' in a company. Future Quality companies are those which will attain and sustain high returns on investment. ESG considerations are integral to Future Quality investing as good companies make for good investments. In our most recent Future Quality Insights article we provide examples of how Future Quality companies approach environmental and social factors in a way that benefits all stakeholders.

The four pillars used to assess the Future Quality characteristics of an investment are as follows:

Franchise – does the company have a sustainable competitive advantage?

Management – does the company make sound strategic and capital allocation decisions?

Balance Sheet – is growth appropriately financed?

Valuation – are the company's prospects under-appreciated by the market?

We believe that investing in Future Quality companies will lead to outperformance over the full market cycle. Our strategy is based on fundamental, bottom-up research therefore sector and country allocations are a function of stock selection. The Global Equity strategy is a concentrated, high conviction portfolio with a high active share ratio.

Market Review

Global markets have recorded one of their largest opening quarter returns in a long time, with global equities rising by 10.29% in Q1, offsetting most of the losses of Q4 2018. The main driver was investors growing increasingly confident that the US rates had peaked and that global trade conflicts were likely to ease.

With such a strong start to the year, it naturally leads investors to question whether further gains are likely. The debate is even more evident when you consider the continued wealth of negative revisions – German PMI, earnings downgrades, etc. - and the inversion of US rates which occurred after the last Federal Reserve (Fed) meeting towards the end of the March.

As economic data has continued to soften over March, renewed monetary dovishness has been evidenced everywhere. Monetary stimulus is increasing in China and the European Central Bank is once again emphasising the downside risks to economic growth – talking of renewed support for the region's beleaguered banking sector.

At the time of writing, a resolution to the trade war between China and the US remains uncertain. However, markets appear to be pricing a benign outcome as a number of more cyclical stocks have bottomed out, or even starting to perform positively. An acceleration in growth in the second half of 2019 is currently being debated. The inversion of the US yield curve has led the US banking sector to underperform in a meaningful way and investors have sought safety in defensive stocks like the ones from the utilities sector. We have limited exposure to these sectors but they do provide informational value such as investor’s appetite for risk. The strategy has benefited from this as strong results and the hunt for safety have led investors into holdings such as Verisk and Ecolab.

Leadership in equity markets was fairly broad in Q1, with information technology and real estate rising 16.80% and 14.03%, respectively. Energy also saw relatively strong returns of 12.19%—a reversal from Q4 2018 when it was one of the weakest performing sectors. One of the heaviest underperformers in Q1 was healthcare (6.20%) and financials, which suffered as a result of the US yield inversion, although still returned a positive 6.39%.

Market Outlook

As we enter the second quarter of 2019, there are a number of themes that have provided good Future Quality stocks for the portfolio, and these are unchanged from last quarter. These include:

Value-based Healthcare — demographics fuel growth in demand for healthcare services. They are also part of the problem, as an increasing number of people live longer, with more chronic illnesses. The need for public providers to deliver care for these conditions as efficiently as possible will only become more pressing.

China — while rising trade tensions, tighter bank lending and shifting Chinese economic imperatives continue to weigh on some economic sectors, others remain better placed. We still believe that businesses that offer the building blocks for the long-term economic development of China offer attractive growth.

Cloud computing and the Industrial Internet of Things — we remain very selective when investing in the technology sector – in recognition of stretched valuations and the blurring of cyclical / structural growth that these often reflect. We are still willing to invest in areas where we can see a genuine path to long-term growth, allied with strong current cash flow generation. Cloud computing and some of the capabilities that this supports (such as machine learning), possess these attributes.

With cheap financing abundant over the last decade, there is an above-average number of plausible sounding new technologies and businesses available to investors at present. The IPO of Lyft at the end of March is such an example. Although we are likely to see more of these unicorn IPOs, suspect class share structures and losses into the foreseeable future mean these companies struggle to meet our Future Quality threshold.

We remain optimistic that the excesses that have heralded the last recessions are generally absent however we believe that the long-term impact of quantitative easing remains unclear at this stage. What is clear, is that volatility is likely to remain high and the sharp reaction of equity investors to US monetary normalisation certainly suggests that the global economy is not yet ready for this support to be removed. We do, however, believe that the economic environment will be more testing in the near future and strong management will be key if companies are to thrive. This should play well for the pillars that underpin Future Quality investing.

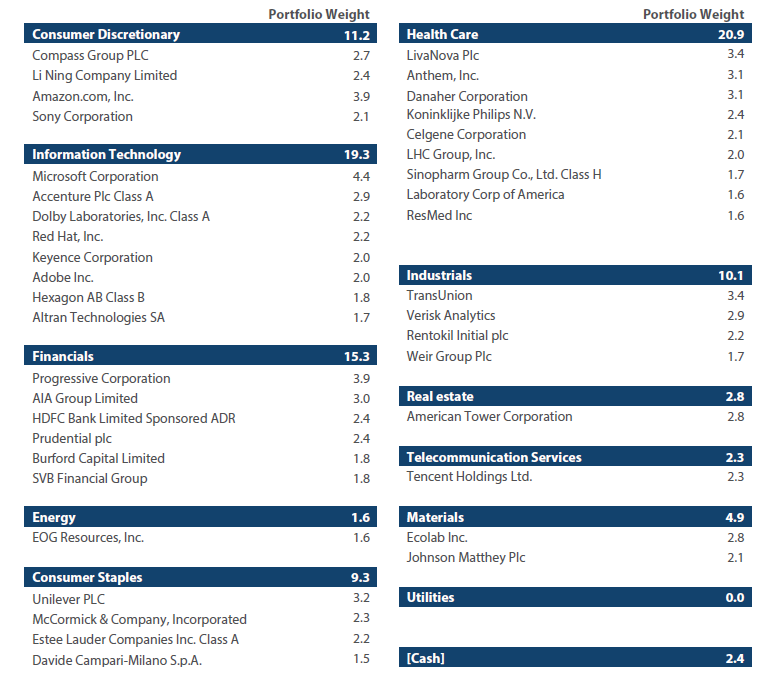

Portfolio positioning

The table below highlights our Global Equity Strategy holdings as of the end of March 2019.

The holdings shown above are based on a representative account managed by the investment team. Reference to individual stocks does not guarantee their continued inclusion in the portfolios managed by the team. Any references to particular securities are for illustrative purposes only and are as at the date of publication of this material. This is not a recommendation in relation to any named securities and no warranty or guarantee is provided.

Source: Nikko AM, FactSet as at 31 March 2019

Global Equity Strategy Composite Performance to Q1 2019

Cumulative Returns October 2014 to March 2019

Past performance is not indicative of future performance.

Source: Nikko AM, FactSet, Bloomberg

The track record for Nikko AM portfolio is based on a composite portfolio from 01 October 2014 to 31 March 2019. *The benchmark for this composite is MSCI AC World Index. The benchmark was previously the MSCI All Countries World Index ex AU since inception of the composite to 31 March 2016. Returns are US Dollar based and are calculated gross of advisory and management fees, custodial fees and withholding taxes, but are net of transaction costs and include reinvestment of dividends and interest.

*The track record for SWIP is based on a composite portfolio managed by the investment team whilst at SWIP from 31 March 2011 to 31 March 2014. The team was subsequently acquired by Nikko AM in August 2014. The benchmark for this composite was the MSCI World Index.

Nikko AM Global Equity Team

This Edinburgh based team provides solutions for clients seeking global exposure. Their unique approach, a combination of Experience, Future Quality and Execution, means they are continually ‘joining the dots' across geographies, sectors and companies, to find the opportunities that others simply don't see.

Experience

Our five portfolio managers have an average of 22 years' industry experience and have worked together as a Global Equity team for eight years. They have recently recruited an analyst, who is the first appointment of a new generation of talent to the team. The team's deliberate flat structure fosters individual accountability and collective responsibility. It is designed to take advantage of the diversity of backgrounds and areas of specialisation to ensure the team can find the investment opportunities others don’t.

Future Quality

The team's philosophy is based on the belief that investing in a portfolio of 'Future Quality' companies will lead to outperformance over the long term. They define 'Future Quality' as a business that can generate sustained growth in cash flow and improving returns on investment. They believe the rewards are greatest where these qualities are sustainable and the valuation is attractive. This concept underpins everything the team does.

Execution

Effective execution is essential to fully harness Future Quality ideas in portfolios. We combine a differentiated process with a highly collaborative culture to achieve our goal: high conviction portfolios delivering the best outcome for clients. It is this combination of extensive experience, Future Quality style and effective execution that offers a compelling and differentiated outcome for our clients.

About Nikko Asset Management

With US$ 214 billion* under management, Nikko Asset Management is one of Asia's largest asset managers, providing high-conviction, active fund management across a range of Equity, Fixed Income, Multi-Asset and Alternative strategies. In addition, its complementary range of passive strategies covers more than 20 indices and includes some of Asia's largest exchange-traded funds (ETFs).

*Consolidated assets under management and sub-advisory of Nikko Asset Management and its subsidiaries as of 31 March 2019.

Risks

Emerging markets risk - the risk arising from political and institutional factors which make investments in emerging markets less liquid and subject to potential difficulties in dealing, settlement, accounting and custody.

Currency risk - this exists when the strategy invests in assets denominated in a different currency. A devaluation of the asset's currency relative to the currency of the Sub-Fund will lead to a reduction in the value of the strategy.

Operational risk - due to issues such as natural disasters, technical problems and fraud.

Liquidity risk - investments that could have a lower level of liquidity due to (extreme) market conditions or issuer-specific factors and or large redemptions of shareholders. Liquidity risk is the risk that a position in the portfolio cannot be sold, liquidated or closed at limited cost in an adequately short time frame as required to meet liabilities of the Strategy.