Beyond the conflict, we see solutions

by Johnny Russell

It has been 50 years since the start of what is locally called ‘The Troubles’—a civil war in Northern Ireland that over a 30-year period lead to the death of over 3,500 people and injured or killed just under 2% of the population. Northern Ireland is where I call home and where I grew up. Despite The Troubles, I have wonderful memories of my childhood. Was I just lucky? Like life itself, the answer is a little complicated.

My first stroke of luck was my parents’ decision to move out of West Belfast. As things turned out, that decision improved my chances of survival by a factor of almost three-to-one (there were 623 Troubles-related deaths in West Belfast vs 213 in South Belfast). My second stroke of luck was the school my parents chose to send me to. Both of my parents worked in mixed communities with Catholics and Protestants and decided on a school that offered children, regardless of religion or colour, loads of opportunity.

I now realise my parents had a set of values; a framework for how they wanted to bring up their children. Both my parents worked hard and neither earned a lot of money. What was earned was funnelled into a family home—a safe one at that. That purpose, and the values underpinning it, drove their key decisions in life.

Source: Shutterstock

We all have multiple roles in life—parent, child, spouse, coach, colleague, friend, teammate, leader—and for most of us, each role needs to be worked on and nourished.

If I devote all my time and effort to any one of these areas, the others suffer. And while it may work out in the short term, over the long term my overriding goals will be lost. Like many things in life, things are complicated and there is a need for balance.

Businesses are similar. They need a purpose and a framework of values to deliver that purpose—something other than just maximising profits.

Profits are a construct to help measure how successful a company is solely through the eyes of the shareholder. In fact, it is the singular focus on profit at the expense of all other stakeholders that has led to our current state, where the success of capitalism is being questioned.

As it happens it is also 50 years since Nobel Prize-winning economist Milton Friedman won the debate on the role of businesses with his view that their only responsibility is to maximise profits. But the Friedman doctrine is starting to be rejected in favour of a model that considers all stakeholders.

The overarching pursuit of profit maximisation, which is underpinned by the notion of self-interest, has lowered the purpose of business and robbed many firms of their ability to engage with communities, employees and others. As a result, trust in capitalism is on the wane.

The purpose of business is not to maximise short-term profits. It has always been to provide profitable solutions for society’s problems. To do this they need to consider all stakeholders and find purpose and value for each in the pursuit of these solutions.

The environment in which companies operate and indeed the assets owned by companies have significantly changed over the last 50 years. More is currently being invested in intellectual property and research and development. There is a greater recognition that businesses are using natural resources without recourse. It is becoming clearer that companies need to consider a broader list of stakeholders if they are to succeed.

A good example of failing to consider the impact of their stakeholders is Ryanair. Europe’s largest airline has delivered cheap travel to the masses. For many years, the firm benefitted from profitable growth and a rising share price, resulting in a happy investor base. However, this was at a cost.

The management team and in particular its CEO, Micheal O’Leary, is well known for cutting costs and adding surcharges onto customer fares. However, this ultimately led to a number of profit warnings in 2018 after their cabin crew and pilots went on strike or left to join the competition. Their singular approach and unhappy employee base remains an issue today.

To achieve sustainable profit growth, all stakeholders need to buy in to the company’s mission if the company is to deliver that value. If not, the business will flounder.

(For reference: we held Ryanair between September 2014 and June 2018, during which it delivered a positive contribution of 2.08%. We sold it as we believed returns had peaked and the pilot strike would impact profits.)

Source: Shutterstock

One Globe – Many Cultures

One of the joys of covering global equities is the opportunity to meet people from different countries and learn about their cultural differences. These differences can influence how companies are managed and consequently how we approach our investments and engage with management teams.

Our search for Future Quality leads us to companies that we believe will attain and sustain high returns. With the influence of multiple stakeholders on the rise, how management teams deal with these shifting tides will impact future returns. These areas simply can’t be ignored.

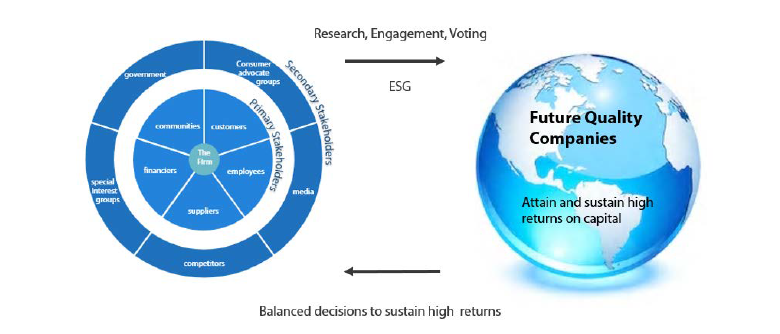

Nikko AM’s Approach to Stakeholder Analysis

Source: Nikko AM, Stakeholder Theory Diagram—Firm Centric. Based on R. Edward Freeman

The Friedman doctrine is more a Western approach to value creation which has evolved to where management teams have not been held to account and the pursuit of profit—as opposed to the company’s mission or purpose—has dominated all else.

Some cultures have never been as enthusiastic about the Friedman doctrine. For example, in Japan there is greater emphasis on creating shared value for all stakeholders, as demonstrated by the following excerpt.

Kazuno Inamori, founder of Kyocera, mentors 5,000 leaders of small-to-midsize companies through a management school called Seiwajyuku. Here is what he teaches them:

“I tell them to seek profits by doing the right thing as a human being. No company can generate long-term profit unless it makes every stakeholder happy. Altruism will bring a company the right profit and long-term growth. I encourage business leaders to keep their own compensation reasonable and manage their business with altruism. They contribute not only to themselves but also to the people around them. Top executives should manage their companies by earning reasonable profits through modesty, not arrogance, and taking care of employees, customers, business partners and all other stakeholders with a caring heart. I think it’s time for corporate CEOs of the capitalist society to be seriously questioned on whether they have these necessary qualities of leadership.’

Source: 13D, ‘What I Learned this Week’, 13 April 2009

This isn’t suggesting that there are no Japanese companies struggling to properly consider all of their stakeholders. However, such Japanese firms tend to face different environmental, social and governance (ESG) challenges, which mainly relate to governance, inefficient balance sheets and demographic headwinds.

We believe the long-term trend away from Friedman towards a more balanced approach to creating value is permanent. However, identifying the companies that will benefit from this shift is not easy. Management teams are aware of the changes in society, however, the growth in ESG—for example, growth in related assets, research providers, sustainability reports and Sustainable Development Goals (SDG)—has also led to widespread ‘greenwashing’.

Despite challenges to determine authentic engagement with employees and communities, we have identified a number of companies that have elevated their purpose and placed stakeholders at the core of their strategy. One such example is Unilever.

Case Study: Unilever and ‘Benefit Corp’ Status

As a global leader in fast-moving consumer goods, Unilever has relied on its powerful brands and strong distribution channels to deliver solid growth and high returns on capital for many years. Our assessment as to whether this success is sustainable into the future hinges on our assessment of the franchise quality of the business.

For companies who rely on consumers around the world buying their products daily, doing the right thing from an environmental, social and governance perspective is increasingly synonymous with long-term strength of individual brands. Having the right products, manufacturing and distributing them in the right way, and benefiting all stakeholders in the value chain are critical ingredients in the creation of long-term value. Unilever, with its range of purpose-driven brands, is an excellent example of a company achieving these objectives.

With 2.5 billion people worldwide using Unilever’s products every day, the company understands that to thrive long term, they need to serve society the right way today. Unilever’s sustainability plan not only mitigates risk but is a driver of profitable growth. The firm’s objective is to grow profitably while reducing its environmental impact by half, thereby improving the health and well-being of more than 1 billion people and enhancing the livelihood of millions of others in its value chain. This is a blueprint for long-term value creation with compounding growth. As long-term investors, we believe Unilever is a prime example of a quality company today, as it ensures that its brands sustainably deliver against stakeholder expectations of value creation. It is truly a Future Quality company.

We believe these initiatives are central to the sustained quality of Unilever’s returns on capital. Indeed, the company points out that their ‘brands driven by purpose’ grew 60% faster than their traditional brands in 2018. ESG factors are no longer just mitigators of risk, they are genuine drivers of franchise quality for the business and one of the key factors by which we assess Future Quality at the stock research level.

Source: Unilever Investor Relations, CAGNY conference February 2019

The clearly identifiable and measurable targets Unilever has put in place stands as testament to the high quality of the management team and their commitment to pursue United Nations SDGs while continuing to profitably grow their business.

The evidence of the need for change is everywhere: global populist movements, rising wealth divides and a younger generation that increasingly believes the system is rigged against it. Scores of companies now tout their ESG credentials, but few have gone the extra mile to gain externally accredited Benefit Corp (B Corp) status, thereby matching their processes with long-term thinking and the creation of shared value. Unilever has seven businesses with B Corp status, such as Ben & Jerry’s Ice Cream and Pukka Herbs.

There are now over 2,750 certified B Corps across 150 industries and 64 countries. The direction of travel is set and management teams are reacting to society’s changing needs.

Conclusion

“Not everything that counts can be counted and not everything that can be counted counts.”

—Albert Einstein

The blinding focus on short-term profit maximisation at the expense of everything else has damaged the role capitalism needs to play in solving society’s problems. As with individuals or the family unit, fulfilment is not measured by net worth. Without purpose and an understanding of how stakeholders are impacted, companies will continue to give in to short-term pressures and ultimately may lose their license to operate.

Whether it’s the scale of share buy backs, the low level of wages as a percentage of profits, the increase in importance of ESG across the asset management industry, increased inequality, social unrest or Larry Fink’s annual letter to Blackrock’s shareholders, the focus on a wider base of stakeholders is a trend that is here to stay.

Increasingly we are seeing businesses interject purpose and stakeholder analysis into board room discussions. This is a positive trend as capitalism needs a new narrative; one that reflects its true purpose and ability to deliver value to society as well as to its shareholders. Capitalism has successfully solved many of society’s problems in the past and we think good management teams are already on the journey to showing that this trend will continue.

Brexit – And Bargain Hunting

Voting for Brexit was billed as ‘taking back control’. But since the referendum, the pound sterling has fallen about 17% against the UK’s major trading partners and recent corporate activity on the London Stock Exchange suggests that the UK is up for sale.

This year alone, announced public-to-private deals have exceeded USD 30 billion, with a wide range of targets: media content, domestic pub chains, a defense contractor and real estate companies, among others. Data compiled by Datalogic shows that, since 2016, there have been over 3,000 mergers and acquisitions of UK companies—about 50% more than in the previous three years.

And the falling pound sterling isn’t the only reason for this activity. The booming private equity world is as much to blame, with perhaps as much as USD 750 billion (per Preqin, the data provider) looking for an investment. And this dry powder sees value in the UK.

We have identified undervalued, high-return businesses in the UK for some time, so this change in heart by foreign buyers comes as no surprise. As we approach a conclusion to Brexit, perhaps we are past peak uncertainty? And why past the peak?

Well it’s back to Northern Ireland. The fear of a return to The Troubles’ should lead all parties to find a solution to Northern Ireland’s border with Europe. Let’s hope so.

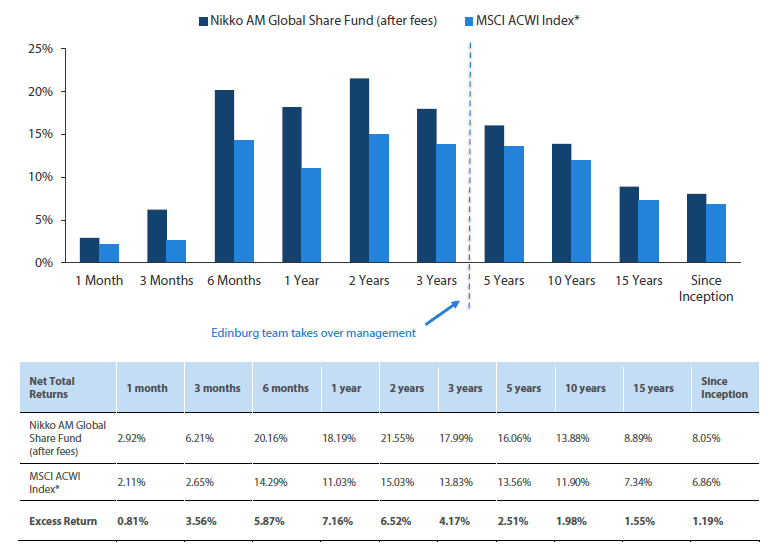

Nikko AM Global Share Fund Performance to 31 July 2019

In July 2015, the Nikko AM Global Share Fund was restructured from a global equities multi-manager strategy to gaining this exposure by investing in the Nikko AM Global Equity Fund, which is a sub-fund of the Nikko AM Global Umbrella Fund, an open ended investment company registered under Luxembourg law as a SICAV. The Nikko AM Global Equity Fund is managed by the Nikko AM Global Equity team based in Edinburgh.

Source: BNP Paribas & Nikko AM. Total fund returns are post -fees, pre-tax, using redemption prices and assume reinvestment of distributions. Past performance is not an indicator of future performance. As at 31 July 2019. *Benchmark: MSCI All Countries World Index (with net dividends reinvested) expressed in Australian Dollars (unhedged) Prior to 18 August 2016, the Benchmark was MSCI All Countries World Ex-Australia Index (with net dividends reinvested) expressed in AUD (unhedged). Prior to 15 July 2015 the Benchmark was the MSCI World ex-Australia Index (with net dividends re-invested) expressed in AUD (unhedged). Prior to 1 October 2005, the index was the MSCI World Index (net dividends reinvested) expressed in AUD (unhedged). Inception date: November 1995

Nikko AM Global Equity Team

This Edinburgh based team provides solutions for clients seeking global exposure. Their unique approach, a combination of Experience, Future Quality and Execution, means they are continually ‘joining the dots’ across geographies, sectors and companies, to find the opportunities that others simply don’t see.

Experience

Our five portfolio managers have an average of 22 years’ industry experience and have worked together as a Global Equity team for eight years. They have recently recruited an analyst, who is the first appointment of a new generation of talent to the team. The team’s deliberate flat structure fosters individual accountability and collective responsibility. It is designed to take advantage of the diversity of backgrounds and areas of specialisation to ensure the team can find the investment opportunities others don’t.

Future Quality

The team’s philosophy is based on the belief that investing in a portfolio of ‘Future Quality’ companies will lead to outperformance over the long term. They define ‘Future Quality’ as a business that can generate sustained growth in cash flow and improving returns on investment. They believe the rewards are greatest where these qualities are sustainable and the valuation is attractive. This concept underpins everything the team does.

Execution

Effective execution is essential to fully harness Future Quality ideas in portfolios. We combine a differentiated process with a highly collaborative culture to achieve our goal: high conviction portfolios delivering the best outcome for clients. It is this combination of extensive experience, Future Quality style and effective execution that offers a compelling and differentiated outcome for our clients.

About Nikko Asset Management

With USD 224 billion* under management, Nikko Asset Management is one of Asia’s largest asset managers, providing high-conviction, active fund management across a range of Equity, Fixed Income, Multi-Asset and Alternative strategies. In addition, its complementary range of passive strategies covers more than 20 indices and includes some of Asia’s largest exchange-traded funds (ETFs).

*Consolidated assets under management and sub-advisory of Nikko Asset Management and its subsidiaries as of 30 June 2019.

Risks

Emerging markets risk - the risk arising from political and institutional factors which make investments in emerging markets less liquid and subject to potential difficulties in dealing, settlement, accounting and custody.

Currency risk - this exists when the strategy invests in assets denominated in a different currency. A devaluation of the asset's currency relative to the currency of the Sub-Fund will lead to a reduction in the value of the strategy.

Operational risk - due to issues such as natural disasters, technical problems and fraud.

Liquidity risk - investments that could have a lower level of liquidity due to (extreme) market conditions or issuer-specific factors and or large redemptions of shareholders. Liquidity risk is the risk that a position in the portfolio cannot be sold, liquidated or closed at limited cost in an adequately short time frame as required to meet liabilities of the Strategy.

Important Information

This material has been prepared by Nikko Asset Management Europe Ltd (