Inspiration from Eddie

By Iain Fulton

Until a few days ago, we had never heard of Edwina Brocklesby or her inspirational story. “Eddie”, as she prefers to be known, spent 50 years as a UK-based social worker. After retiring, Eddie became a CEO, author and triathlete. At age 50 she took up running and has spent the last 25 years competing in marathons, triathlons and Ironman races across the globe. In 2018, aged 74, Brocklesby became the oldest British athlete to complete the Ironman distance and she has plans to complete another Ironman event in the summer of 2020 at the tender age of 76. Her book Iron Gran: How Keeping Fit Taught Me that Growing Older Needn't Mean Slowing Down is proof that it’s never too late to start—particularly as many of us struggle to keep up the good intentions we may have had at the start of a new year.

Source: Shutterstock

Aside from being an inspirational athlete, Eddie Brocklesby gained a PhD in 2007 and founded a charity named Silverfit in 2013. Silverfit is led by older people, for older people and promotes happier, healthier ageing through physical activity while combatting social isolation. Its “sandwich” formula sessions involve socialising, light exercise then socialising again.

The programme is allowing its members to reduce medication and attend their GP's surgeries less often due to increased fitness and social inclusion. For her services to healthy ageing, Eddie was awarded the British Empire Medal and still has plans (and the energy) to expand the Silverfit charity across the UK.

Such inspirational stories about achievements in later life and the ways communities often come together to tackle social problems are so easy to lose sight of in today's world. Our newsfeeds are constantly jammed up with the latest threat to life as we know it and let's face it, investors would be forgiven for having lost track of the news over the last few weeks. In such a short time, the US and Iran seemed on the brink of war, impeachment proceedings were ongoing against the US president, the UK left the EU, the bushfire environmental crisis continued in Australia and a high profile business executive allegedly escaped from Japan in a box. And then there is the coronavirus… and earnings season. What should investors do to separate signal from the noise in a period of such uncertainty?

Ageing requires solutions

Similar to Eddie Brocklesby's charity Silverfit, our job as investors is hopefully to help people enjoy a healthier and happier retirement. By focusing on the long term qualities of the businesses we invest in, we aim to help our clients achieve their financial goals which in many cases can relate to financial security later in life. This long term horizon is particularly important during periods of uncertainty.

The Silverfit story reminds us of the social challenges we face when it comes to an ageing society. There is clearly a view that the overall cost of healthcare provision today is unsustainable and that steps need to be taken to improve outcomes while reducing the financial burden. The Silverfit initiative is a perfect example of how communities can take action to address an obvious problem. We believe businesses that can achieve the same goal by helping solve enduring problems, such as the costs of healthcare, pension deficits or climate change are more likely to be great investments. Companies will increasingly have to be part of the solution rather than part of the problem.

Solution providers come in many forms

When picking companies, we are looking for businesses that can deliver the required solutions and do so profitably. Future high returns on invested capital is a key measure for us as it encourages reinvestment, an essential requirement for the long duration over which we need to address problems, such as healthcare affordability and retirement savings.

LHC Group, the largest provider of in-home nursing care in the US, is an excellent example of a company addressing the healthcare affordability challenge. Caring in a home environment is both preferred by recipients and more cost effective, and when a company has a proven model of delivery that is both competitive and high quality, market share growth is the outcome.

Another long-standing holding for us is Philips—an equally excellent example of a company we seek that is on the path to Future Quality. Philips has evolved from an industrial conglomerate to a business that is solely focused on excellence in a range of healthcare solutions. One particular solution is connected healthcare, where innovative hardware and software is enabling patient monitoring in the home, rather than in the elevated cost environment of hospitals.

Source: Shutterstock

The development of new therapies for a variety of health-related issues is undertaking a rapid expansion due to developments in biotechnology, gene sequencing and artificial intelligence. Bio-Techne, a new holding in the latest quarter, is a leading provider of protein products and immunoassays that form the building blocks of genomics research. The picks and shovels of this new gold rush are more likely to be franchises that deliver enduring returns rather than the inevitable creative destruction of single product firms that are currently being funded by cheap capital.

Getting old comes at a cost and for individuals that usually requires a combination of savings and insurance to cope. But obtaining compound returns in a low yield environment is a major challenge, driving the need for cost-effective but quality insurance in both developed and emerging markets.

Holdings in the portfolio that are delivering such solutions include AIA, a leading provider of life insurance in many emerging markets, and Anthem, one of the leading healthcare insurance providers in the US. While Progressive Insurance, a notable position in the portfolio, may not be specifically targeted at older customers seeking auto or home insurance, its ongoing market share growth highlights its superior business model that delivers cost-effective solutions and savings that can be directed productively elsewhere.

Our hope is that the businesses mentioned and others held in the portfolio can provide the products and services to help the new generation of "Iron Grans" meet their goals.

Fires and plagues

As far as earnings season is concerned, we’ve been encouraged by the continued strong growth and good profitability coming from companies in the cloud infrastructure industry. Amazon’s AWS and Microsoft’s Azure businesses are showing rapid growth with very good margins. With only 3% of overall IT budgets currently directed to the cloud, we think the long-term prospects for continued growth and good returns on capital are strong.

In the consumer sector, those businesses with direct exposure to travel retail in Asia have understandably downgraded their expectations given the decline in passenger numbers and a heavily disrupted Lunar New Year period. The market is largely treating this as a temporary phenomenon, just as investors did with the SARS outbreak in the early 2000s. Only time will tell if this is the correct approach.

More alarmingly, we have been struck by the impact and the scale of the bushfires that have devastated so many communities in Australia in recent weeks. It would appear difficult to underplay the role climate change has in this and other extreme weather events around the world. It also appears that this has brought us to a social, economic and political tipping point where issues related to climate change become central to policies and actions that, historically, were marginalised and put off for a distant point in the future.

Investors now appear to be allocating capital more aggressively to those businesses that are part of the solution rather than part of the problem. Industries are also realigning. Within industrials, Woodward (a provider of technologies to improve industrial engine efficiency) announced a merger with Hexcel (the leading provider of lightweight aerospace materials). This new company is solely focused on providing its customers with a set of solutions that reduce emissions and the carbon footprint of its industry. If they can achieve this objective, we feel the long-term prospects for further market share gains and improved profitability are strong.

Source: Shutterstock

Finally, observant readers will be aware that this month’s author normally rides the train to work. This particular “mobility-as-a-service” takes about 25 minutes and covers roughly 19 miles of picturesque Scottish coastline from Fife to Edinburgh. The line is a little busier now than it was a couple of years ago when we began this publication and there are more electric vehicles parked at the station than there once were. A trend which clearly seems set to continue. To play my part while also invoking a bit of Iron Gran’s spirit, I’m going to swap the train for my running shoes tomorrow and run that 19 mile journey into work. Please don’t be afraid, two of us on the global equity team are in late stage preparations for a spring marathon so hopefully we’ll be ok. Proof indeed that it’s never too late to start.

Reference to individual stocks is for illustration purpose only and does not guarantee their continued inclusion in the strategy’s portfolio, nor constitute a recommendation to buy or sell.

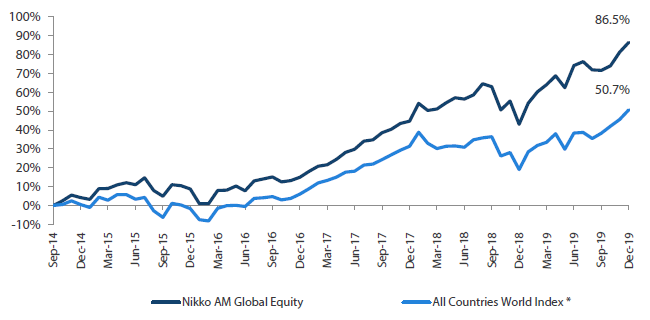

Global Equity Strategy Composite Performance to Q4 2019

Cumulative Returns October 14 to December 19

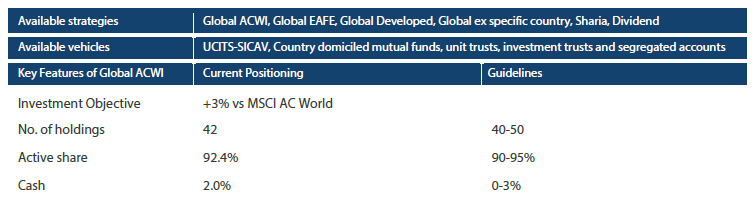

Nikko AM Global Equity: Capability profile and available funds (as at 31 December 2019)

Past performance is not indicative of future performance.

This is provided as supplementary information to the performance reports prepared and presented in compliance with the Global Investment Performance Standards (GIPS®). Nikko AM Representative Global Equity account. Source: Nikko AM, FactSet.

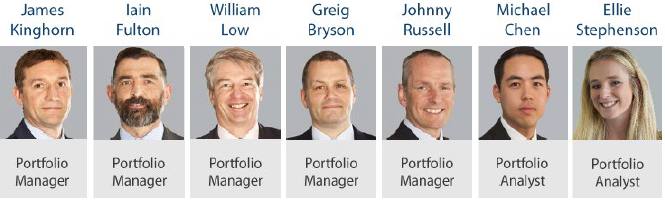

Nikko AM Global Equity Team

This Edinburgh based team provides solutions for clients seeking global exposure. Their unique approach, a combination of Experience, Future Quality and Execution, means they are continually “joining the dots” across geographies, sectors and companies, to find the opportunities that others simply don’t see.

Experience

Our five portfolio managers have an average of 23 years’ industry experience and have worked together as a Global Equity team for eight years. In February 2019, Michael Chen joined the team and later in September Ellie Stephenson joined the team as Portfolio Analysts. They are the first in a new generation of talent, on the path to becoming Portfolio Managers. The team’s deliberate flat structure fosters individual accountability and collective responsibility. It is designed to take advantage of the diversity of backgrounds and areas of specialisation to ensure the team can find the investment opportunities others don’t.

Future Quality

The team’s philosophy is based on the belief that investing in a portfolio of “Future Quality” companies will lead to outperformance over the long term. They define “Future Quality” as a business that can generate sustained growth in cash flow and improving returns on investment. They believe the rewards are greatest where these qualities are sustainable and the valuation is attractive. This concept underpins everything the team does.

Execution

Effective execution is essential to fully harness Future Quality ideas in portfolios. We combine a differentiated process with a highly collaborative culture to achieve our goal: high conviction portfolios delivering the best outcome for clients. It is this combination of extensive experience, Future Quality style and effective execution that offers a compelling and differentiated outcome for our clients.

About Nikko Asset Management

With USD 246.5 billion* under management, Nikko Asset Management is one of Asia’s largest asset managers, providing high-conviction, active fund management across a range of Equity, Fixed Income, Multi-Asset and Alternative strategies. In addition, its complementary range of passive strategies covers more than 20 indices and includes some of Asia’s largest exchange-traded funds (ETFs).

*Consolidated assets under management and sub-advisory of Nikko Asset Management and its subsidiaries as of 31 December 2019.

Risks

Emerging markets risk - the risk arising from political and institutional factors which make investments in emerging markets less liquid and subject to potential difficulties in dealing, settlement, accounting and custody.

Currency risk - this exists when the strategy invests in assets denominated in a different currency. A devaluation of the asset's currency relative to the currency of the Sub-Fund will lead to a reduction in the value of the strategy.

Operational risk - due to issues such as natural disasters, technical problems and fraud.

Liquidity risk - investments that could have a lower level of liquidity due to (extreme) market conditions or issuer-specific factors and or large redemptions of shareholders. Liquidity risk is the risk that a position in the portfolio cannot be sold, liquidated or closed at limited cost in an adequately short time frame as required to meet liabilities of the Strategy.