Last month saw a marked increase in share price volatility in some of the stocks deemed most insulated from the adverse impacts of COVID-19. We suspect that this volatility will persist for some time as the real strengths of economies are revealed; with emergency wage support measures rolling off in the UK, inventories partially rebuilt and political uncertainty elevated.

Global equity investment philosophy

Our philosophy is centred on the search for “Future Quality” in a company. Future Quality companies are those that we believe will attain and sustain high returns on investment. ESG considerations are integral to Future Quality investing as good companies make for good investment. The four pillars we use to assess the Future Quality characteristics of an investment are:

Franchise—does the company have a sustainable competitive advantage?

Management—does the company make sound strategic and capital allocation decisions?

Balance Sheet—is growth appropriately financed?

Valuation—are the company’s prospects under-appreciated by the market?

We believe that investing in Future Quality companies will lead to outperformance over the full market cycle. Our strategy is based on fundamental, bottom-up research therefore sector and country allocations are a function of stock selection. The Global Equity strategy is a concentrated, high conviction portfolio with a high active share ratio.

Market outlook

One factor that has been helping equity markets push higher in recent months has been positive earnings revisions. Given the unprecedented nature of the coronavirus outbreak and the economic lockdowns introduced to limit its spread, it is not surprising that forecasting error has turned out to be significant for estimates compiled back in the dark days of March to May this year. Hindsight is a wonderful thing in investment, but it turns out that the world hasn’t yet ended and that people still need and want to do the things that give them pleasure.

Where will profit expectations go from here and how realistic are expectations that 2021 will mark a return to pre COVID-19 normal? These questions look especially pertinent as we near the traditional flu season in the northern hemisphere and deal with increasing infection rates. Can the public health risks be effectively managed without jeopardising economic health? At the very least, politicians should no longer be under any illusion regarding the economic damage done by lockdowns. The societal damage and the disproportionately high burden of this damage on those worse off in society should be equally clear.

Our portfolio has experienced more than its fair share of strong performers throughout the crisis, despite none of us foreseeing the virus. Dealing with the virus has just accelerated changes that were already taking place; be it the migration of data to the Cloud, the enabling of more flexible working or the shift of some healthcare out of hospitals and into patients’ own homes. In each case, we believe that these changes address major societal issues and will persist long after vaccines have successfully been developed and the threat posed by the coronavirus has passed. The sustained nature of the growth opportunities that these changes present for Microsoft, Amazon, Adobe, LHC Group and Encompass Health (among others), are not yet fully reflected in the stocks’ long-term valuations. Nevertheless, we have taken profits in some stocks in recognition of them pulling forward of demand. We have been investing the proceeds to increase positions in companies that have been tagged COVID-19 losers, but where we remain confident in their long-term Future Quality credentials, even if we acknowledge that we have no way of knowing when the challenges posed by the vaccine will pass. Compass Group and HDFC are good examples.

The successful development and commercialisation of vaccines for the virus remains the most likely clearing event that would trigger a re-evaluation of the merits of these two camps. Data continues to accumulate on the efficacy and safety of the many products in development. Recent commentary by both regulators and the drug industry suggest that they will not be swayed by the political calendar when assessing their vaccines. This may not help the Republican Party (or those wishing for a rally into year-end) but is almost certainly the best approach to eradicating the threat posed by the virus in the long term. Last month saw a marked increase in share price volatility in some of the stocks deemed most insulated from the adverse impacts of COVID-19. We suspect that this volatility will persist for some time as the real strengths of economies are revealed; with emergency wage support measures rolling off in the UK, inventories partially rebuilt and political uncertainty elevated. We remain optimistic that the picture will look reasonably positive—at least by the middle of next year. With other asset classes looking more expensively valued than equities, we remain constructive on markets. Most importantly, the current bifurcation of markets between the COVID-19 haves and have-nots is continuing to present attractively valued Future Quality businesses for us to invest in on behalf of our clients.

Portfolio positioning

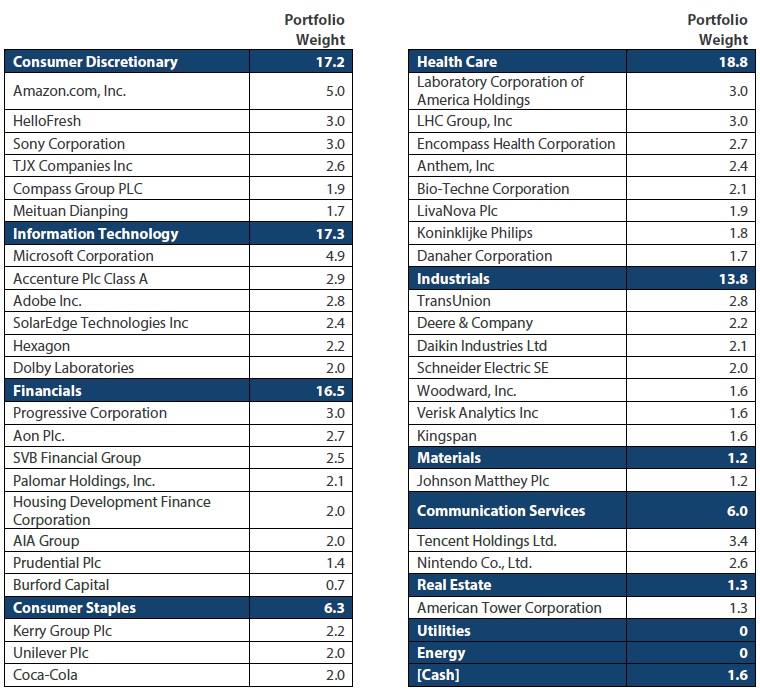

The table below highlights our Global Equity Strategy holdings as of the end of September 2020.

Reference to individual stocks is for illustration purpose only and does not guarantee their continued inclusion in the strategy’s portfolio, nor constitute a recommendation to buy or sell.

Global Equity Strategy Composite Performance to Q3 2020

Cumulative Returns October 14 to September 20

*The benchmark for this composite is MSCI All Countries World Index. The benchmark was the MSCI All Countries World Index ex AU since inception of the composite to 31 March 2016. Inception date for the composite is 01 October 2014. Returns are based on Nikko AM’s (hereafter referred to as the “Firm”) Global Equity Strategy Composite returns. Returns for periods in excess of 1 year are annualised. The Firm claims compliance with the Global Investment Performance Standards (GIPS ®) and has prepared and presented this report in compliance with the GIPS. Returns are US Dollar based and are calculated gross of advisory and management fees, custodial fees and withholding taxes, but are net of transaction costs and include reinvestment of dividends and interest. Copyright © MSCI Inc. The copyright and intellectual rights to the index displayed above are the sole property of the index provider. For more details, please refer to the performance disclosures found at the end of this document. Data as of 30 September 2020.

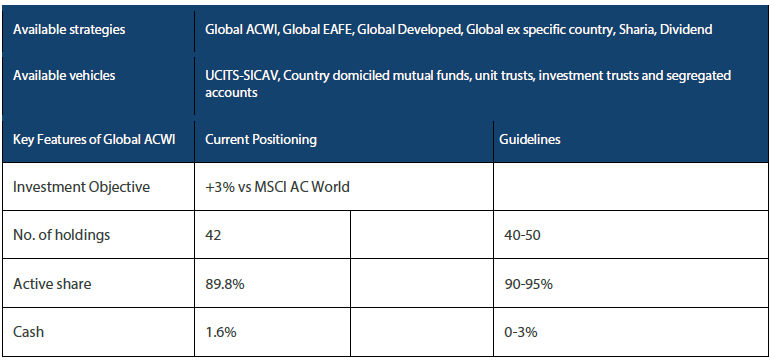

Nikko AM Global Equity: Capability profile and available funds (as at 30 September 2020)

Past performance is not indicative of future performance. This is provided as supplementary information to the performance reports prepared and presented in compliance with the Global Investment Performance Standards (GIPS®). Nikko AM Representative Global Equity account. Source: Nikko AM, FactSet.

Nikko AM Global Equity Team

This Edinburgh based team provides solutions for clients seeking global exposure. Their unique approach, a combination of Experience, Future Quality and Execution, means they are continually “joining the dots” across geographies, sectors and companies, to find the opportunities that others simply don’t see.

Experience

Our five portfolio managers have an average of 23 years’ industry experience and have worked together as a Global Equity team for eight years. In 2019, two portfolio analysts, Michael Chen and Ellie Stephenson joined the team and they are the first in a new generation of talent on the path to becoming portfolio managers. The team’s deliberate flat structure fosters individual accountability and collective responsibility. It is designed to take advantage of the diversity of backgrounds and areas of specialisation to ensure the team can find the investment opportunities others don’t.

Future Quality

The team’s philosophy is based on the belief that investing in a portfolio of Future Quality companies will lead to outperformance over the long term. They define Future Quality as a business that can generate sustained growth in cash flow and improving returns on investment. They believe the rewards are greatest where these qualities are sustainable and the valuation is attractive. This concept underpins everything the team does.

Execution

Effective execution is essential to fully harness Future Quality ideas in portfolios. We combine a differentiated process with a highly collaborative culture to achieve our goal: high conviction portfolios delivering the best outcome for clients. It is this combination of extensive experience, Future Quality style and effective execution that offers a compelling and differentiated outcome for our clients.

About Nikko Asset Management

With USD 249.5 billion* under management, Nikko Asset Management is one of Asia’s largest asset managers, providing high-conviction, active fund management across a range of Equity, Fixed Income, Multi-Asset and Alternative strategies. In addition, its complementary range of passive strategies covers more than 20 indices and includes some of Asia’s largest exchange-traded funds (ETFs).

*Consolidated assets under management and sub-advisory of Nikko Asset Management and its subsidiaries as of 30 September 2020.

Risks

Emerging markets risk - the risk arising from political and institutional factors which make investments in emerging markets less liquid and subject to potential difficulties in dealing, settlement, accounting and custody.

Currency risk - this exists when the strategy invests in assets denominated in a different currency. A devaluation of the asset's currency relative to the currency of the Sub-Fund will lead to a reduction in the value of the strategy.

Operational risk - due to issues such as natural disasters, technical problems and fraud.

Liquidity risk - investments that could have a lower level of liquidity due to (extreme) market conditions or issuer-specific factors and or large redemptions of shareholders. Liquidity risk is the risk that a position in the portfolio cannot be sold, liquidated or closed at limited cost in an adequately short time frame as required to meet liabilities of the Strategy.