Snapshot

With the US presidential election now behind us, the two candidates seem to be proceeding in parallel universes. The apparent winner, President-elect Joe Biden, has transition planning and inauguration on his mind while President Donald Trump continues to challenge the election process itself. Nonetheless, one thing is clear: the so-called “blue wave” in which the Democrats overwhelmingly take the White House and flip the Senate majority has failed to materialise. Although the Senate race is seemingly close, the Republicans are still likely retain their majority following runoffs for two seats in January 2021. In positioning terms, the blue wave has been closely associated with the “reflation trade” as another large US fiscal stimulus package would drive bond yields higher and prompt a rotation from growth to value stocks. As the markets readjusted to a different outcome in the few days following the election, growth stocks initially outperformed value on the back of compressing bond yields.

While the Trump campaign continues to pursue its legal options to challenge the election, Biden will also face a divided government even if his win is confirmed. A divided government will likely put the Democratic agenda in a gridlock and cloud the party’s near-term plan for a major pandemic relief package, which was a key impetus for the reflation trade. Even if Trump does manage to win somehow, the outcome is much the same—more limited stimulus. We expect market positioning to remain in a state of flux as the election result has not delivered a “clear” winner yet and sporadic news on COVID-19 vaccines will create cross currents for investors to navigate. Over the near term, value stocks will attempt to wrestle leadership in global equities from growth stocks while US Treasury yields will remain volatile. Emerging markets may give back some of their recent outperformance, but China might benefit from a Biden administration, with few expecting the same degree of aggression Trump applied in fighting the trade and technology war.

But is the reflation trade over? We don’t think so. While a blue wave promised larger and faster fiscal spending, stimulus is still on the horizon whether from a Biden or Trump administration and, importantly, monetary policy remains very supportive. Also, fiscal and monetary policy continues to be supportive in the rest of the world while demand—particularly from China—continues to improve. COVID-19 headwinds remain, including recent lockdowns in Europe, but we still believe the world is learning to live with the virus, and the normalisation in demand will only accelerate next year should a vaccine become available. Over the longer term, we believe these reflationary conditions still support a weaker dollar, higher yields and some degree of rotation from growth to value.

Cross-asset1

We are sitting tight and remain neutral on growth assets while shifting marginally negative on defensive assets. As US election risk continues to recede, some form of new fiscal stimulus will be forthcoming whether Biden is confirmed or President Trump retains office. This will prove to be non-threatening for global growth assets and steepen the US yield curve as new stimulus comes into view. Meanwhile, the pandemic has seen a resurgence across the US and Europe as the northern hemisphere enters the colder winter months. While there are pockets of lockdowns to contain the virus, broad economic shutdowns are still highly unlikely given that most cases are among the young and thus mortality rates have stayed low.

US demand has remained resilient despite the delay of Phase IV stimulus and any new disappointments on the prospects for fresh fiscal spending is still a clear watch point. Among growth assets, we stay neutral on developed market (DM) and emerging market (EM) equities while marginally reducing REITs in favour of Infrastructure given that the former is more exposed to further shutdowns. On the defensive side, we reduced sovereign bonds and investment grade credit in favour of inflation assets, given the reflationary environment that coordinated expansionary monetary and fiscal policy are targeting. And finally, we have maintained our neutral scores for both growth and defensive currencies.

1The Multi Asset team’s cross-asset views are expressed at three different levels: (1) growth versus defensive, (2) cross asset within growth and defensive assets, and (3) relative asset views within each asset class. These levels describe our research and intuition that asset classes behave similarly or disparately in predictable ways, such that cross-asset scoring makes sense and ultimately leads to more deliberate and robust portfolio construction.

Asset Class Hierarchy (team view1)

")

1The asset classes or sectors mentioned herein are a reflection of the portfolio manager’s current view of the investment strategies taken on behalf of the portfolio managed. The research framework is divided into 3 levels of analysis. The scores presented reflect the team’s view of each asset relative to others in its asset class. Scores within each asset class will average to neutral, with the exception of Commodity. These comments should not be constituted as an investment research or recommendation advice. Any prediction, projection or forecast on sectors, the economy and/or the market trends is not necessarily indicative of their future state or likely performances.

Research views

Growth assets

The growth outlook is still nuanced with some risks receding while others rising to take their place, mainly due to the pandemic resurgence. Typically, growth assets price far out into the future, but in our COVID-19-stricken world, few are willing to price that future until the end of the pandemic is in sight. Moreover, even in a post-pandemic world, can we count on demand behaviours returning to pre-pandemic norms? In some cases, such as commercial real estate or business travel, clearly not. But the degree of shifting demand behaviours remains an unknown.

Currently, we remain focused on election risk, which has diminished. But more importantly, we are now also focused on governments and their attempts to balance virus-countering economic shutdowns with economic growth. We do remain cautious, but ultimately believe that governments will not entertain extended shutdowns early next year.

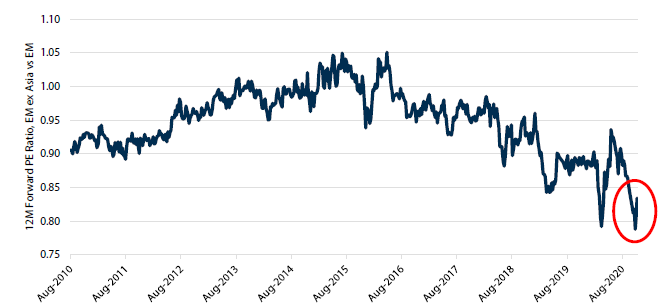

EM ex-North Asia turning a corner?

There are probably few asset classes which have been as hard hit as EM ex-North Asia this year. Governments in these countries largely failed to contain the virus and had limited fiscal resources to stimulate domestic demand while external demand for their commodity exports faltered. New economy sectors such as technology and internet are also lightly represented in these regions, leaving opportunities few and far between. Not surprisingly, equities from these regions have been punished while valuations have recently hit historical lows.

Chart 1: EM ex-Asia valuation relative to broad EM

Source: Bloomberg, October 2020

However, in the aftermath of the US election and promising vaccine news in early November, a stunning rally took place with MSCI ASEAN, EMEA and LatAm outperforming their broad EM benchmark by as much as 8.5% within a few days. Could the global backdrop be turning more favourable for them? Probably yes is our view for a few reasons. Deep value often rests on deep uncertainty, which only needs to be moderately reduced to trigger a powerful rally. US election uncertainty is mostly over, while a vaccine looks to be on the horizon to help demand normalise.

Has uncertainty ended? Certainly not, given the new virus outbreaks in Europe and the US; furthermore, it is unclear when the vaccine can be approved, and considerable time could be needed before it can be distributed broadly. Still, an end to the pandemic appears to be in view and investing in potential beneficiaries that are currently very cheap is sensible. Meanwhile, while recent outbreaks are likely to weigh on the demand recovery, fiscal policy remains supportive and monetary policy remains even more so, lasting at least through next year. Overall, the worst for EM ex-North Asia looks to be ending with prospects much brighter amid hopes for the vaccine’s eventual arrival.

However, not all EM ex-North Asia are created equal. The early dash for low credit assets—which lifted even Argentina bonds—is likely to give away to differentiation, with quality exposures continuing to be rewarded while low quality exposures are likely to resume their struggle.

Conviction views on growth assets

- Holding the barbell: this month we made modest changes to the basket, keeping tech in the US and North Asia balanced with a value proposition in Europe and Japan and a neutral position so far for the rest of emerging markets.

Defensive assets

Global central banks continue to pledge support for markets and encourage governments to maintain supportive fiscal spending as the pandemic rolls on. While the size of any new fiscal package in the US may be uncertain following the election, we expect the Congress to approve further pandemic relief spending regardless of the final election outcome. As a result, government bond yields are likely to trend higher as this reflation push ultimately succeeds over the pandemic with help from prospective vaccines. This leads us to slightly downgrade our view on sovereign bonds this month.

We continue to prefer investment grade credit over government bonds. Credit spreads recovered from the modest widening last month, narrowing to the tightest levels since the pandemic began. While spreads are unlikely to fluctuate much from these levels, upward pressures on global benchmark yields will be a headwind for returns.

Inflation assets top our defensive asset classes following an upgrade this month. The case for inflation protection is rising as global central banks commit to easy policies until data sustainably improves (and on standby if more is needed) and governments continue to increase fiscal spending as the pandemic lingers. The combination of high savings rates and rapid progress towards a vaccine could lead to higher inflation in 2021.

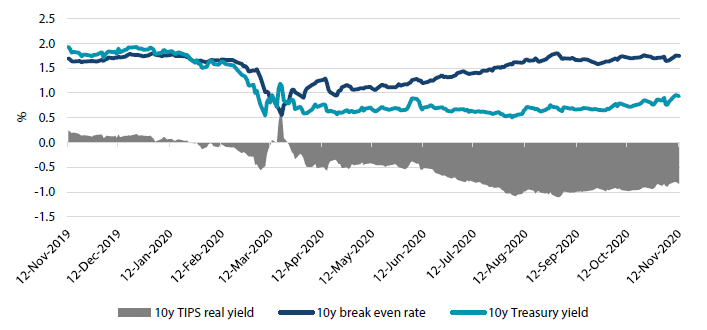

Challenges ahead for US Treasuries

The world’s largest central banks have taken aggressive action using both monetary policy and quantitative easing in response to the pandemic. They have pledged to maintain these accommodative policies until a sustained recovery takes hold and realised inflation rises to meet or exceed targets. In addition, central banks have called upon governments to use fiscal spending to complement their actions and this advice has largely been heeded. We expect that this substantial and synchronised monetary and fiscal support will be successful in carrying the global economy through the pandemic until vaccines can be widely distributed in the first half of 2021. As a result, investors will increasingly look ahead to an improving global economy and rising inflationary pressures that will begin to steepen global yield curves and curtail returns from sovereign bonds.

The pacesetter in global bond markets, 10-year US Treasuries (UST), had already started to weaken ahead of the US election and this trend has continued post-election despite rising COVID-19 cases. As we consider what the higher end of the UST yield range may look like over the next three to six months, we are keeping an eye on real yields and break-even inflation rates. The Federal Reserve (Fed) has been quite transparent in wanting to maintain easy monetary conditions while encouraging higher inflation in order to meet its “symmetric” inflation goal of 2%. As a result, we expect the Fed will want to keep 10-year real yields firmly negative (our expectation is a range of -0.5% to -1%) and see break-even rates trending higher to at least 2%. Combining a real rate of -0.5% and break-even inflation rate of 2% results in a UST yield of about 1.5%, which is where we would expect the top of the range to be. While any sudden and rapid move higher in UST yields would likely draw in the Fed to support the market, we think it will be comfortable with higher UST yields over time as long as break-even inflation rates are rising as well.

Chart 2: US real rates and break even inflation

Source: Bloomberg, November 2020

As the outcome of the US election is becoming clearer, Biden and the Democratic Party are highly likely to pursue further fiscal support even if it proves to be a scaled-down version of their ambitious package proposed before the election. This additional fiscal spending will also require greater Treasury issuance. However, we expect the Fed to increase its bond buying programme to significantly offset any increase in supply. In our view, UST yields are likely to rise due to increasing inflation pressures rather than on supply concerns.

There are two main risks to our outlook. The first risk is the US presidential election process not being able to deliver a “victor”, leading to period of extreme uncertainty about the formation of the next US administration. However, such a risk seems to be fading. As of this writing, President-elect Biden’s lead continues to grow in the most important battleground states. The second risk is setbacks in efficacy trials damaging expectations for a COVID-19 vaccine to be developed in the near-term. The news, however, has been positive so far and researchers appear to be making significant headway in proving an effective and safe vaccine. If even one these risks were to eventuate, USTs would likely perform their usual safe haven role and yields would fall, contrary to our outlook.

Conviction views on defensive assets

- Take the spread in IG credit: Credit spreads continue to offer an attractive yield premium that will drive credit outperformance over sovereign bonds.

- Steeper yield curves ahead: We expect yield curves to steepen as investors increasingly look ahead to a strong global recovery in 2021 driven by coordinated monetary and fiscal policy and successful vaccines.

Process